Dec 27, 2021

According to recent research for BBC Panorama, a typical family in the UK is likely to spend £33.60 more each week during 2022 because of inflation. This adds up to £1700 per year!

The research was based on a range of prices, including:

Looking at the above list, there seems no way of avoiding having to pay out more money. Which is a daunting prospect, especially if you are already in debt.

So perhaps it’s time to tackle those debts once and for all? Imagine being debt-free by the end of 2022!

This may sound like an impossible dream. But with some time and effort – and also professional help if needed – it can begin to happen sooner than you may think.

In this article we suggest a six step plan that will help you to get on top of your debts during 2022.

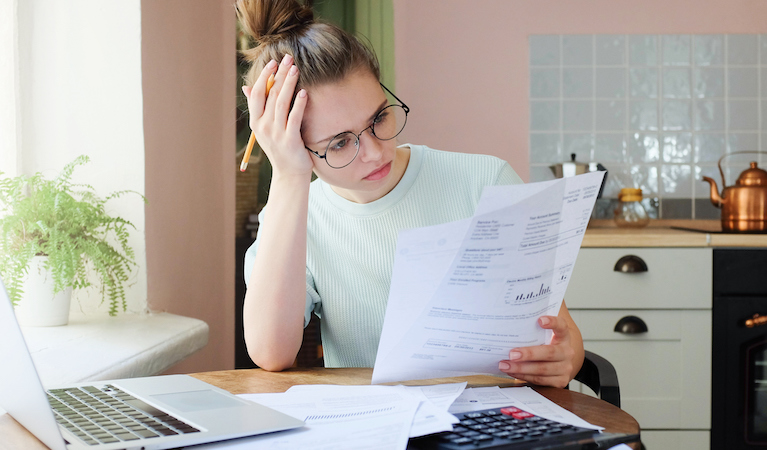

The first step to really tackling debt is to understand the scale of the problem. In fact many people get tied up in debt because they are scared to do just this. A little bit like the ostrich with its head in the sand, it just seems easier if we don’t know, and we somehow hope it will all go away by itself. But it won’t.

So the first thing to do is to make a list of all your debts. Include everything you owe, including loans, overdrafts and credit cards. They may add up to a frighteningly large total. But that total exists whether or not you acknowledge it. The important thing now is to decide how you are going to tackle it.

There are now three steps to take:

If you have a lot of debts and are finding it hard to keep track, you may want to consider taking out a short term loan to pay them all off and just have one monthly repayment to make.

This can be hard to do, but once your debts are paid off you will have more disposable income and can start saving again.

One of the reasons many people slide into debt is that they live outside their means and overspend each month. It is so easy to do. Perhaps they end up using up more and more of their overdraft allowance each month, then begin to pay for essentials on credit cards, which then means more expense each month to make credit card payments. And so it goes on.

So the key to getting out of debt is to make a realistic monthly budget and stick to it. You need to start by making two lists:

First of all a list of how much money you think you spend on everything in a typical month. This is your expenditure. It needs to include:

Then make a list of your monthly income i.e. all the money coming into the household each month. For example salary or wages, tips, bonuses, and benefits.

Once you have these two lists, you will be able to see clearly whether you have enough money to manage each month, or whether you are likely to continue building up debt.

At this point, there are two additional things you can do to help you sort your budget out:

But what do you do if, after doing all the above, you realise you don’t have enough income to cover your expenditure? How do you balance your budget?

The key thing NOT to do is pile up more debt. It can be tempting to keep spending using your overdraft or credit cards. But this will only make things worse.

At this point, don’t panic, but try to view your debt situation as a challenge to be overcome. It can be helpful to look online for inspiring blogs and vlogs about how different people have sorted out their debts. You will feel less isolated, and will be encouraged that it is possible to do this.

In simple terms, you need to take a three-pronged approach to your financial situation:

Find any legal way to make more money. Even if this is tough, keep telling yourself it’s only for a short while. Perhaps a sacrifice is worth it to get you back on your feet again.

Some of the ways that other people have done this include:

Do everything you can to spend less money. There are many ways to do this without significantly changing your lifestyle. Check out some of our earlier articles for hints and tips on how to reduce spending and save money.

As well as generally reducing expenditure, perhaps each month you could decide not to spend money on one particular category of non-essential items, such as we mentioned earlier. Just cutting out one little luxury per month could help towards balancing your budget.

Also make it one of your resolutions for 2022 not to use credit cards at all unless it is a genuine emergency.

Any time you have any spare money, for any reason, pay it straight into your debts. This will feel a bit unfair at times, but the sooner you ditch the debts, the sooner you can begin to enjoy life again without always worrying about money.

Even if you just manage one of these balancing acts for a short while, you will gradually start to see a difference in your finances. But if you can do two or, ideally, all three of the above, things will start to resolve much more quickly.

Do you want the good or the bad news?

The good news is that, for most people, a concerted effort along the above lines will soon start to make inroads into your debts and help you along the way to a healthier financial future.

The bad – or at least not so good – news is that you can’t let up. You have to keep going. It can take years of bad money habits to get into serious debt and start seeing it as a normal part of life. So it is not all going to change overnight.

The best thing to do is to keep going through Steps 1-4 again and again, until your debts are completely cleared. But even then it is still really important to stick to Step 4 – Balancing your Budget – so that your spending doesn’t get out of control again and debts start to rebuild.

Which is all well and good. But what if you do try the above steps, but feel you are in such a financial mess that you can’t get out of it?

The good news here is that there are people who can help you. Let’s take a look . . . .

If after trying the above you still feel totally overwhelmed by your debts, it may be time to seek external help. A good place to start is Money Helper – a free and impartial money advice service set up by the government that can point you in the right direction.

Other debt advisory services include:

With the help of a debt professional you may be able to make arrangements with your creditors to delay, reduce or even cancel some of your debts, for example through a debt management plan or Individual Voluntary Arrangement (IVA).

So never feel that there is no-one to turn to: help is out there if you need it.

We hope that this article helps you to find ways to deal with your debts in 2022.

Check back here soon for more financial and lifestyle tips from Loans 2 Go.

What to Do If an Unexpected Expense Hits This Summer

What to Do If an Unexpected Expense Hits This Summer